Cannabis consumers pay around $8 a gram, on average. But how much does the grower actually get?

A licensed producer (LP) grows the cannabis. For non-flower products this LP – or a contracted third party – processes the cannabis into a pre-roll, vape, beverage, edible, etc. After that, with some provincial and territorial variance, the products move through a government-run wholesale purchaser, which then fulfils orders to retailers and, in some instances, directly to consumers.

However, there are many processes within this chain, all of which add to the cost. These include laboratory testing, packaging, and shipping. When all of this is taken into account, according to the most recent data from CannStandard, the price of one gram of dried cannabis, from any package size, is $8.54. Given that at the start of legalization in Canada, in October 2018, the price was $11.33, this represents a 25% decrease. But even this may be optimistic.

“CannStandard’s numbers look high to me,” says Dan Sutton Founder and CEO of Tantalus Labs, which is BC’s largest locally-owned and operated LP. “We work off of the metric of duty paid landed wholesale cost, which is averaging under $4.50 a gram – across all packaging volumes – at this time. This is about 50% lower than wholesale prices at the outset of legalization.”

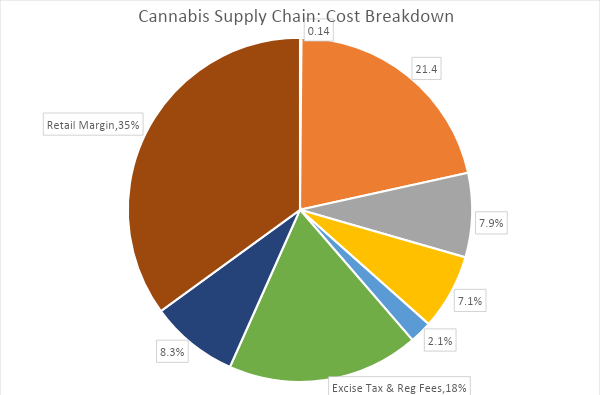

Sutton is one of the driving forces behind the Stand For Craft campaign, which is advocating for excise tax relief in Canada. Stand For Craft has come up with a detailed breakdown of the baked-in cost of a gram of Cannabis in Canada. According to Stand For Craft, a $7 gram would break down as follows: producer margin, $0.01; cultivation and processing costs, $1.50; lab testing costs, $0.55; packaging costs, $0.50; shipping, $0.15; excise taxes and regulatory fees, $1.26; provincial distribution tariff, $0.58; retailer margin, $2.45.

When looking at this data on a percent basis, the breakdown looks like this:

A few things stand out when looking at this data. The first is the difficulty in assessing what is going on with LPs, which are reluctant to discuss margins. Given the hundreds of millions of dollars that the big LPs have lost over the past three years, it is fair to say that some are operating with negative margins in a desperate attempt to unload flower and gain market share.

Of course, smaller craft providers are feeling this squeeze, too. However, there is anecdotal evidence, provided to StratCann by retailers off the record, that some higher quality flower is developing a loyal brand following, and are able to command premium prices.

The greatest variable in the data appears to be in cultivation/processing and packaging. This is where leading companies are investing in order to build brand loyalty, yet there are major cost differentials depending on the product.

“For the most part, for our business and the brand’s business to be successful, they need to know how to recoup from retail,” says Pawel Kruba, Manager, Business Development, at Peak Processing, which helps companies with sourcing and integration, as well as the development of beverages, extracts and concentrates, vapes, powders, and topicals, among other services. “However, each product and brand is format dependent – it is very difficult to speak in general terms.”

What is clear is that processing ups the cost, and that the margins are low. Those companies that order higher volumes have an advantage, as do those that have clear visibility into their costs across the supply chain, and consumer uptake.

“Where we’ve had success is with flavour profiles,” says Kruba. “With beverages, a company can leverage marketing to drive sales, as opposed to just saying ‘This is a 10-milligram beverage that will get you high’.”

The cost of doing business

It costs money to make a quality product, and consumers should keep this in mind, particularly when purchasing in the regulated market, where brands have to stand behind what they deliver. For example, in the unregulated market edibles have been shown to have drastically lower THC levels than advertised. At under 8% of total cost, lab fees would seem to be good value.

By far the biggest bite in the supply chain comes from retailers. The Stand For Craft data, which puts the margins at 35%, is largely consistent with those reported by retailers contacted by StratCann. Some of the retailers, all of whom wanted to be off the record, claimed margins as low as 30%, and it is possible that the big “value chains” – such as Value Buds and Canna Cabana – are working with even thinner margins.

While cultivation and processing represent about 21% of the total cost, it might surprise consumers to know that excise and regulatory fees, at 18%, far exceed the average taken by the provinces, at only 8.3%. In Canada, when cannabis is priced at under $10 a gram, the excise tax on cannabis has a floor set at $1 per gram, which increases the tax margin as a function of revenue.

As well, the excise and regulatory fees do not include taxes at the point of sale, such as GST and PST. When combined, the consumer is ultimately paying upwards of 30% to some form of government.

Private craft operators have not had access to public markets, which has made it more difficult for them to compete, given that larger firms can operate at a loss for longer periods. This pressure is ongoing, and despite the fact that the price of a gram of cannabis has been in steady decline, the industry is still vulnerable to inflationary pressures across the supply chain.

“Crop inputs have increased in price around 20% over the last year due to increased transportation costs arising from global supply chain crunch through COVID,” says Sutton from Tantalus. “Further to this, supply gaps have created situations where critical inputs are hard to acquire, forcing cultivators to buy larger volumes when they are available, locking up working capital.”

There have been ongoing challenges sourcing cones for pre-rolls. Sutton also notes that packaging costs have increased at least 15%, and shipping times have tripled.

“Shipping costs on all inputs have seen exponential cost increases,” he says. “One supplier increased its shipping cost from $3,000 per container in 2019 to over $15,000 per container in 2022.”

Many of the supply chain pressures are still in place. The many regulatory requirements specific to legally available cannabis – such as lab testing, tariffs and taxation, packaging requirements, the role of provinces, and retail regulation – are unavoidable fixed costs. The irony is that while these may add to the price of cannabis, they also ensure that consumers get exactly what they pay for.