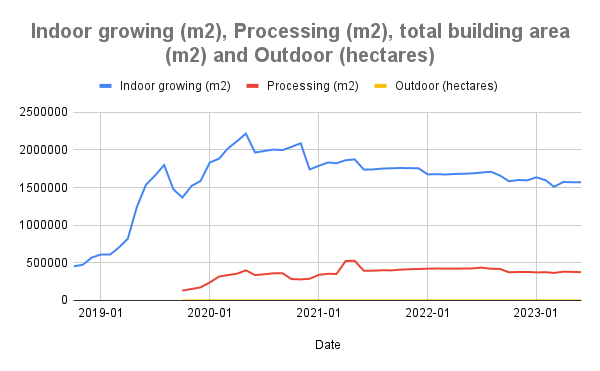

The amount of unpackaged inventory cannabis producers are sitting on has continued to decline from a peak in late 2022, while approved indoor grow space has been slowly declining from a peak in early 2020.

Approved outdoor production space has also declined from a peak in late 2021. Unsurprisingly, the estimated number of people employed on federally licensed cannabis production sites has also been declining from a peak in late 2021.

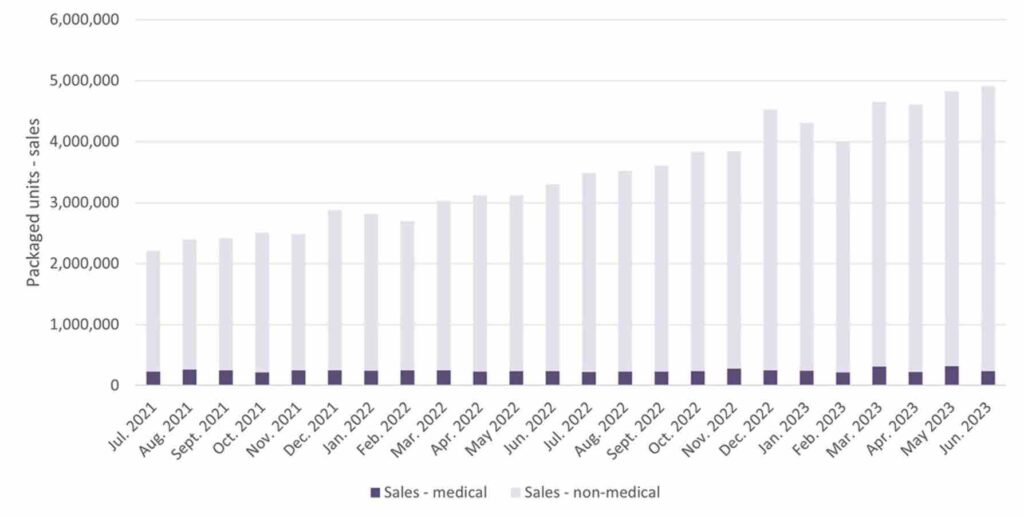

Dried flower still dominates cannabis sales, but cannabis extracts and edibles continue to slowly eat away at that market share.

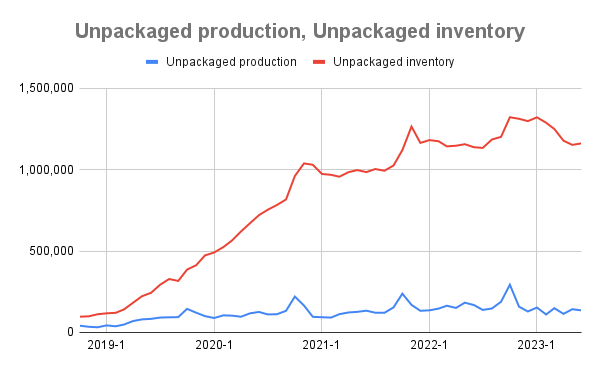

While the volume of unpackaged, dried cannabis flower licensed producers have in their vaults is still over one million kilograms, that amount has been somewhat declining in 2023. The peak volume held by these processors was 1.3 million kilograms in October 2022.

The most recent figures provided by Health Canada, through June 2023, show that figure sat at about 1.2 million, a decline of approximately 161,000 kilograms, or 13%.

While not a significant decline, it does show a trend of a long-standing cannabis surplus beginning to show signs of not only levelling out but even beginning to decline. This surplus of cannabis is a significant reason why prices have been dropping so significantly, often due to larger producers trying to offload large volumes from their vaults at cut-rate prices.

Unpackaged inventory of dried cannabis shows a similar decline, from a peak of 293,188 kilograms in October 2022 to 135,453 kilograms in June 2023. That number dropped even lower, to 110,290 in February of this year, a low not seen since January 2021.

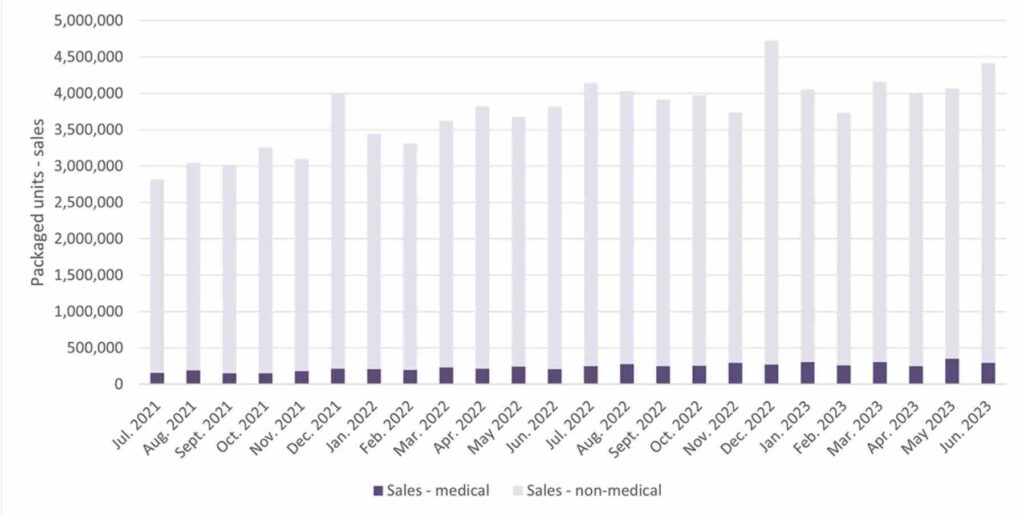

Dried cannabis sales remain the most commonly sold product, with 53% of all medical and non-medical sales in packaged units, compared to 24% cannabis extracts and 22% cannabis edibles.

Cannabis edibles and extracts continue to eat into that market share dominated by dried flower. In October 2020, dried cannabis sales represented 68% of total sales, with 6,989,846 packaged units sold. At the time, edible cannabis sales represented 17% of total sales, while extracts were 15%.

By March 2022, dried cannabis sales represented 58% of total sales, edible cannabis sales represented 23% of total sales and cannabis extracts 19%.

Edible cannabis packaged sales continue to increase year-over-year, with large spikes in December each year. There were 4.4 million packaged units of edible cannabis sold in June 2023, compared to 3.8 million in June 2022 (medical and non-medical).

Packaged sales of cannabis extracts (medical and non-medical) have also been increasing, from 3.3 million in June 2022 to 4.9 million in June 2023. Meanwhile, packaged inventory of cannabis extracts held by producers, as well as provincial distributors and retailers, appears to be settling at around eight to nine million in each category.

Sales of cannabis topicals, which are still a small fraction of the overall market, have also been increasing, with 76,000 packaged units sold in the medical and non-medical stream in June 2023, down from a previous peak in December 2022 of more than 81,000 units sold, and up from June 2022’s nearly 58,000 units sold (medical and non-medical).

However, the total inventory of topicals held by licensed producers, as well as provincial distributors and retailers, has been declining significantly, from a peak of 553,077 units in March 2022 to 333,438 units in June 2023.

The number of non-flowering cannabis plants in Canada’s legal, commercial industry continues to fluctuate seasonally, with spikes in inventory each May or June and declines later in the year. However, while the peak in May 2022 was 3.7 million plants, 3.5 million in June, 2021, and 3.2 million in June, 2020, the high listed amount for 2023 was just over 3 million.

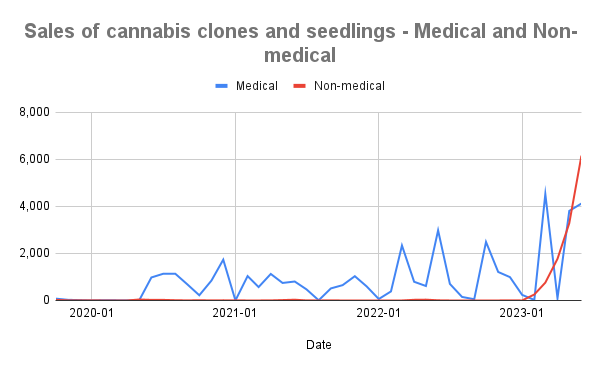

While relatively low, overall, the number of cannabis plants sold in the medical and non-medical channels spiked in 2023 as more cannabis clones made their way into the non-medical “recreational” market. More than 10,000 cannabis plants were sold to medical and non-medical consumers in June 2023, compared to just under 3,000 in June 2022 (and fewer than 1,000 in May and July 2022, respectively).

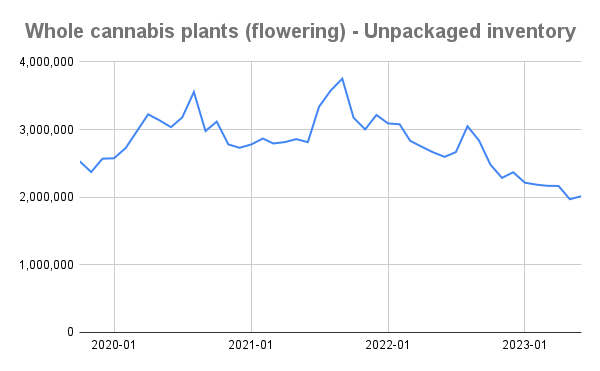

The number of flowering cannabis plants has also declined, from a peak of 3.8 million in September 2022 to 2 million in June 2023.

The total amount of packaged inventory of seeds has also been declining, especially among provincial distributors and retailers, from a previous high of 136,767 packaged units in July 2021 to 59,699 in June 2023.

Sales of cannabis seeds continue to spike in the spring of each year, with 14,459 units sold in April 2022 and 14,784 sold in April 2023. The vast majority of these seeds were sold into the non-medical stream.

100vw, 1024px" />)

100vw, 1024px" />)